economy

innovation

investment

Understanding the West of England’s incubator economy

The West of England has a vibrant start-up economy, but start-up firms and small- and medium-sized enterprises (SMEs) in the region are in a prolonged pattern of cautious investment and deferred growth decisions. As firms mature, value is often captured elsewhere. The priority now is turning early-stage strength into long-term regional value.

This policy insight provides an overview of regional business dynamics across the West of England. It outlines the barriers to growth that start-up firms and SMEs face in Bath and North East Somerset, Bristol, North Somerset and South Gloucestershire. It seeks to understand the reasons behind firm-level behaviours that result in growth and churn across the economy.

The West of England has a vibrant economy, which has seen businesses in the region form and grow over time. This is positive for the region's vitality, as economies have been shown to perform best when there is strong entrepreneurial activity, because the entry of new firms and the exit of old ones keep a region dynamic, innovative and adaptive. As start-ups introduce new technologies and organisational models, less productive incumbents will exit through the process of creative destruction.

This dynamic depends heavily on the strength of local entrepreneurial ecosystems: the interconnected networks of firms, finance, institutions and cultural norms that support innovation, experimentation and business formation (Mason and Brown, 2014; Stam, 2015). These environments enable ‘entrepreneurial recycling’, where experience, capital and knowledge circulate locally, reinforcing innovation and scale-up potential. In this framing, vibrant local churn is not a sign of instability but a mechanism through which regions maintain competitiveness, diversify industrial structures, and raise long-term productivity.

However, innovation ecosystems vary not only in their capacity to generate new enterprises but in their propensity to retain value as those enterprises mature. A region may exhibit high rates of business formation and successful early-stage development while simultaneously experiencing systematic leakage of value through acquisition by external actors.

To understand the West of England's position on this spectrum – and if it functions as a site of sustained value creation or primarily as an incubator for firms that mature elsewhere – requires us to examine both the quantitative indicators of business dynamism and the qualitative mechanisms that shape founder decisions about scaling versus exit.

A closer look at regional business dynamics

The West of England hosts approximately 49,400 enterprises. These are distributed unevenly across the region's constituent local authorities: Bristol accounts for 20,190 firms (41%), followed by South Gloucestershire (10,730 firms) (22%), North Somerset (9,590 firms) (19%), and Bath and North East Somerset (8,855 firms) (18%) (see Table 1). The concentration of businesses in Bristol reflects the city's role as the region's economic centre and its attraction for knowledge-intensive and professional services firms.

Table 1: Business demography by local authority, including weighted regional average, 2023

| Business stock | Micro (%) | Small (%) | Medium (%) | Large (%) |

Bath & North East Somerset | 8855 | 88.2 | 9.9 | 1.4 | 0.5 |

Bristol | 20190 | 86.5 | 11.0 | 2.0 | 0.5 |

North Somerset | 9590 | 89.7 | 8.7 | 1.2 | 0.3 |

South Gloucestershire | 10 730 | 89.0 | 9.2 | 1.5 | 0.4 |

WECA (weighted average) | 49365 | 88.0 | 10.0 | 1.6 | 0.45 |

Source: Office for National Statistics (ONS), 2025, Business demography and UK business datasets; author’s calculations.

The distribution of firms by size in the West of England broadly mirrors national patterns with micro-enterprises (fewer than 10 employees) accounting for 88% of firms in the region. Small firms, with 10-49 employees, make up 10%, while medium firms, those with 50-249 employees, account for 1.6%. Large enterprises with over 250 employees represent under 0.5% of firms in the region. England's figures are comparable at 89% micro, 9% small, 1.5% medium and 0.5% large. This predominance of small firms is characteristic of European economies generally and does not indicate regional or national underperformance.

Within the region, Bristol hosts slightly more scaled enterprises (86.5% micro, 11% small, 2% medium) than the region's average, reflecting its concentration of knowledge-intensive sectors and professional services. South Gloucestershire shows a similar pattern at the medium scale (1.53%), consistent with its aerospace and advanced manufacturing presence, while North Somerset has the highest share of micro firms (89.7%). This is aligned with its orientation toward foundational economy activities.

A healthy scale-up base, but spatial variation in the region is notable

The share of high-growth firms in the region (5.5%) slightly exceeds the England average (5.0%). This confirms a healthy scale-up base and implies that there were roughly 1,000 high-growth firms across the West of England in 2023, approximately three-fifths of which were based in Bristol (see Table 2).

Table 2: Business dynamism indicators by local authority, including weighted regional average, 2023

| Business stock | High-growth (%) | Birth rate (%) | Death rate (%) | Net churn (%) |

Bath & North East Somerset | 8855 | 5.1 | 9.7 | 8.6 | 1.0 |

Bristol | 20190 | 6.1 | 11.2 | 10.7 | 0.5 |

North Somerset | 9590 | 4.9 | 10.8 | 11.0 | – 0.21 |

South Gloucestershire | 10 730 | 5.4 | 10.6 | 10.2 | 0.4 |

WECA (weighted average) | 49365 | 5.5 | 10.7 | 10.3 | 0.4 |

Source: ONS, 2025 Business demography and UK business datasets; author’s calculations.

Note: Net churn = 100 × (births − deaths) ÷ active enterprise stock, using enterprise counts rather than rate differences. Regional values are derived from aggregated births, deaths and stocks across local authorities, consistent with ONS (2025) and OECD (2023) methods.

Bristol has the highest rate of new firms being set up (a 'birth' rate of 11.2%) and largest share of high-growth firms (6.1%), confirming its role as the primary scale-up hub. This concentration reflects broader patterns in the UK's industrial strategy: the UK's eight industrial strategy priority sectors (IS-8), are much more likely to be located in urban areas. Indeed, 32% of UK IS-8 firms are located in city centres (Wang and Swinney, 2025).

Bristol's city-centre professional services cluster exemplifies this pattern. The city also performs significantly above the national average for large cities in attracting frontier industries — those that are high-productivity and research and development (R&D intensive) — such as life sciences, artificial intelligence and digital technologies.

The enterprise birth rate (10.7%) and death rate (10.3%) for the West of England sit just below the average values for England (11.7% and 11.4%), while the resulting net churn (+0.44 percentage points) remains marginally above the figure for England as a whole (+0.3 percentage points).

This indicates slow but steady growth in the business stock. But there is some spatial variation within the region: Bath and North East Somerset shows the most positive net churn (+1.0%), South Gloucestershire aligns closely with the regional average (+0.42%), while the business stock in North Somerset has marginally contracted (−0.2%).

These data describe aggregate patterns of enterprise formation, survival and growth, but it is important to note that not all enterprise creation reflects entrepreneurial ambition for growth. The 88% of regional enterprises classified as micro includes both growth-oriented firms at early stages and established businesses with no intention of scaling. Limited growth ambition should not be conflated with limited economic contribution.

Stability in the region through successive disruptions

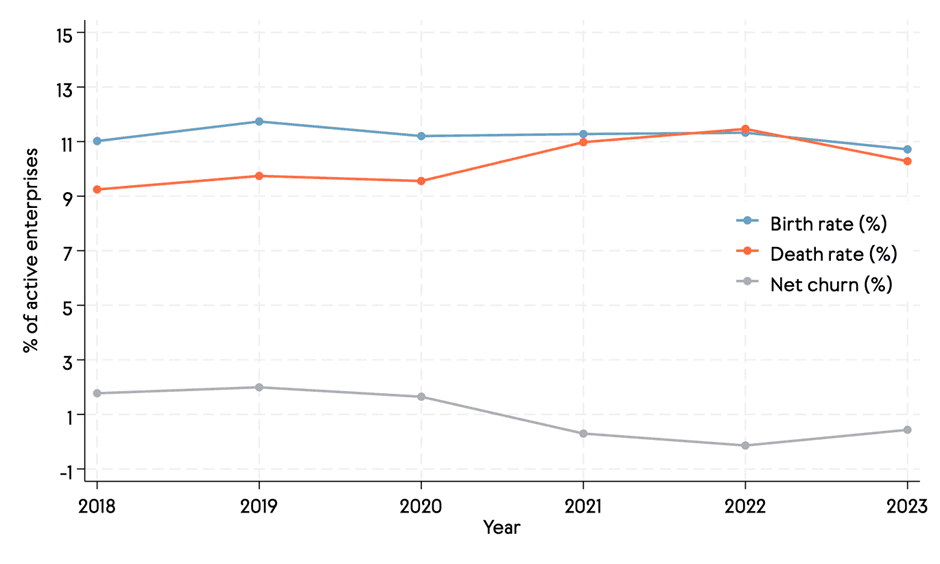

Looking at how enterprise births, deaths and net churn have evolved between 2018 and 2023 provides context for the stability observed in 2023 (see Figure 1).

In 2018-19, start-up activity comfortably exceeded firm closures, producing net churn near +1%. During 2020-21, both formation and exit declined sharply due to pandemic-era uncertainty and government support schemes that suppressed both new entry and business failure, compressing churn toward zero. By 2023, both indicators had normalised at approximately 10-11%, restoring a positive but lower churn level than before the pandemic.

Across local authorities, Bristol remained the most stable; Bath and North East Somerset showed the most year-to-year variation owing to its smaller business base; and South Gloucestershire and North Somerset maintained modest positive churn in most years. The overall pattern is one of mature stability rather than rapid renewal – this is a system that has weathered shocks well but exhibits slower firm-formation momentum than in the late 2010s.

Figure 1: Enterprise births, deaths, and net churn in the West of England, 2018-23

Source: Office for National Statistics (Business demography, enterprise births and deaths by local authority)

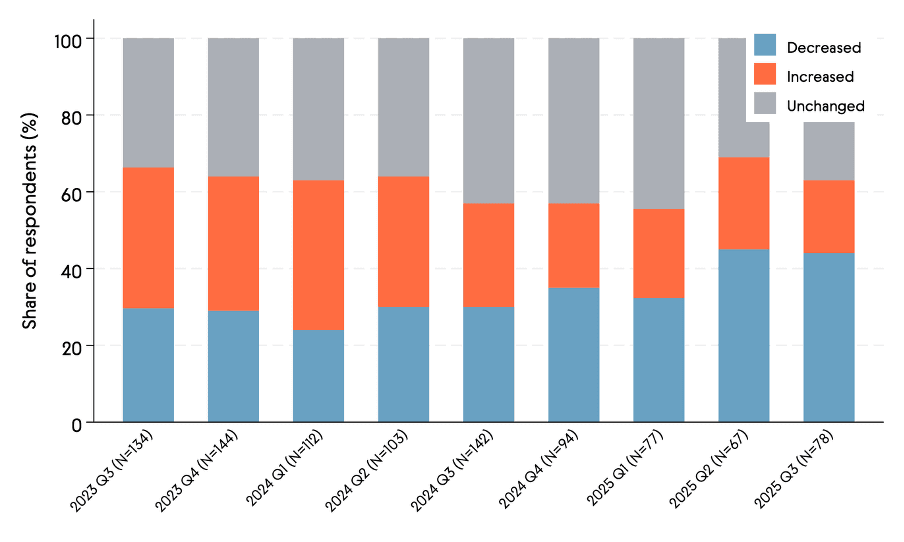

A holding pattern: businesses are maintaining operations without the growth momentum to drive transitions to a larger scale

Firms operating in the West of England are experiencing prolonged stagnation, rather than contraction, according to data from the British Chamber of Commerce's Quarterly Economic Survey. Between 55% and 65% of survey respondents reported unchanged volumes of domestic sales over the period Q3 2023 to Q3 2025 (see Figure 2). The share reporting decreased sales remained relatively contained, though this proportion edged upward throughout 2025.

Figure 2: Domestic sales quarter to quarter in the period Q3 2023 to Q3 2025

Source: Business West (2023-2025) WECA and North Somerset Quarterly Economic Survey Results.

The survey also explores issues of concern for firms in the preceding three months (averaged across Q4 2024 to Q3 2025). In the West of England, general economic conditions were cited by over 80% of respondents while general business uncertainty was mentioned by approximately 70%. These concerns exceed more specific operational pressures, such as taxation, inflation, competition and business rates. Labour market concerns, current financial position and interest rates each registered below 25%.

Financial constraints manifest differently across sectors in the West of England

The primacy of generalised uncertainty over specific cost pressures carries important implications for investment behaviour. Although half of the Quarterly Economic Survey respondents expect investment levels to remain stable, the balance of expectations changed from Q3 2023 to Q3 2025, pointing to a gradual shift toward increasingly defensive investment expectations.

Beyond sentiment and investment intentions, businesses face concrete operational constraints that shape day-to-day decisions about funding, hiring and growth. The three interconnected pressures that emerge from both survey evidence and stakeholder interviews are: access to appropriate finance, workforce-related barriers and navigation of available support.

For example, one interview participant in this research ('Participant C') reported a systematic bias in investment allocation: "There's a huge tech bias within investment for software, I don't think it's particularly a bias against the sector, but more a bias against businesses that aren't directly tech-centred." This observation reinforces that firms within established technology clusters are able to more readily access investment networks than businesses operating in other sectors.

Meanwhile, qualitative evidence from interviews also reveals that activities involved in growing a firm's workforce , such as navigating contracts, workplace regulations and pension auto-enrolment, may present barriers that are most acute at the point of hiring. 'Participant G' observed: “Employing others, that is a minefield for businesses as they grow. … I think that can be a big barrier to growth.”

Acquisition-led exits and the risk of transferring scale-ups elsewhere

What happens when firms are ready to scale up? The evidence suggest that Bristol’s most prominent high-growth firms have exited overwhelmingly through acquisition rather than public listing. Indeed, no recent cases of initial public offering (IPO)-led exits have been identified among high-profile scale-ups in the city (Beauhurst, 2023).

This acquisition-led exit profile contrasts with patterns observed in other UK regions. In Cambridge, university spinouts increasingly pursue public listings, including overseas exchanges, supported by more mature patient-capital networks and institutionalised commercialisation pathways (Cambridge Enterprise, 2025). Manchester exhibits a different model again: the region has produced several homegrown scale-ups that achieved public listings whilst retaining UK headquarters (GM Business Board, 2021). The region's business support infrastructure, centred on The Growth Company and its Business Growth Hub, provides integrated scale-up support encompassing finance, internationalisation, and workforce development (ScaleUp Institute, 2023). Edinburgh, while producing fewer very large scale-ups, benefits from strong entrepreneurial recycling through established angel syndicates and co-investment funds, with local capital repeatedly reinvested into early- and mid-stage firms (Scottish Financial News, 2026).

Interview evidence suggests that exit-oriented development pathways are actively cultivated within the West of England's business support system, not merely tolerated as inevitable outcomes. 'Participant B' noted that founders in technology incubators are "encouraged to think about … what level do they take their company to before they sell it on? Because they're unlikely to be making the final product. They'll be selling on the IP…"

'Participant A' described a similar approach in business support practice: "I learned to support entrepreneurs in understanding… to plan for the point at which they diverge from their business… probably the best outcome is that… they separate, and both thrive without each other... If they've started the business and they're not running the business when it's a thousand-person success story, it's not a failure that they're not the CEO at that point."

These perspectives reflect a pragmatic recognition that founder exit often represents success rather than failure. But when exit typically occurs through acquisition by overseas buyers, the consequences for regional value retention differ markedly from cases where founders exit to local successors or through public listing. This creates an 'incubator economy' risk for the West of England, where the region demonstrates strong capacity for firm creation and early-stage growth, but ownership, strategic control and scaling-up activities are frequently transferred elsewhere through acquisition and relocation.

Conclusion

This new research from the Brunel Centre shows that the West of England’s healthy firm dynamics coexist with an exit-oriented culture that often leads to acquisition-led exits to international buyers. The region’s capacity for firm creation is a strong asset that can support routes for sustainable and inclusive growth, but the current incubator economy dynamic requires interventions and further exploration.

The volume of scale-up activities transferring outside of the region, through acquisitions and relocation, highlights the risk of the West of England being an incubator economy. To maximise the potential of it's healthy start-up base, the policy implication is not to try to convert all micro-enterprises into growth firms, but to ensure that those with growth potential are not impeded by addressable barriers. By developing the region's capacity to support firms to grow and scale while staying put, value can be further retained within the region instead of transferring ownership, IP and control overseas. At the same time the economic and social contribution of businesses that operate sustainably at smaller scale must be recognised.

References

Beauhurst (2023) 'What Makes Bristol Such a Good Startup Ecosystem?', 9 June. Available at: https://www.beauhurst.com/blog/bristol-startup-ecosystem/

Business West (2023-2025) WECA and North Somerset Quarterly Economic Survey Results. Unpublished. Bristol: Business West.

Cambridge Enterprise (2025) Cambridge tops UK for science investment as US capital surges into tech and life sciences. Available at: https://www.enterprise.cam.ac.uk/news/cambridge-tops-uk-for-science-investment-as-us-capital-surges-into-tech-and-life-sciences/

GM Business Board (2021) How Greater Manchester Became the Land of Tech Unicorns and eCommerce Giants. Manchester: Greater Manchester Business Board. Available at: https://gmbusinessboard.com/insights/how-greater-manchester-became-the-land-of-tech-unicorns-and-ecommerce-giants

Mason, C. and Brown, R. (2014) Entrepreneurial Ecosystems and Growth Oriented Entrepreneurship. Background paper prepared for the workshop of the OECD LEED Programme and the Dutch Ministry of Economic Affairs. Paris: OECD.

ScaleUp Institute (2023) ScaleUp Review 2023: Greater Manchester. London: ScaleUp Institute. Available at: https://www.scaleupinstitute.org.uk/scaleup-review-2023/greater-manchester/